I. Introduction

In the global commodity circulation system, packaging has long transcended its function as a mere "container." It has become a critical vehicle for brand identity, user experience, and sustainable development. From the top-and-bottom lid boxes of iPhones to SHEIN's express bags, from IKEA's corrugated furniture to Nongfu Spring's eco-friendly bottle labels, a highly specialized and responsive packaging manufacturing system underpins them all.

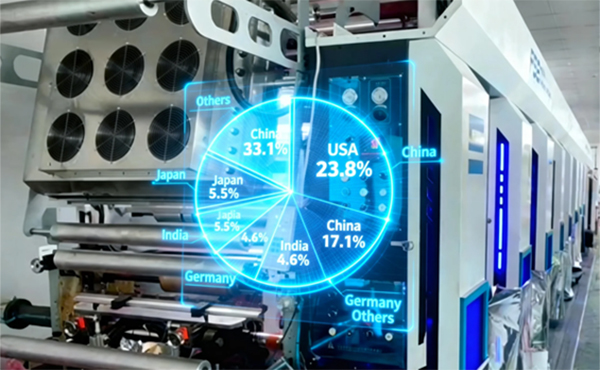

According to the Smithers report "The Future of Global Packaging to 2029," the global packaging market size reached an estimated **$1.05 trillion** in 2024. The Asia-Pacific region accounts for 42% of this, with China firmly holding the top position globally with an output value of approximately **$180 billion** (about 1.3 trillion RMB), representing **over 17%** of the world's total.

Significantly, the **Pearl River Delta (PRD) region contributes nearly 40% of China's total packaging output** — approximately **$70 billion** (Data sources: China Packaging Federation "2024 China Packaging Industry Development Report"; Guangdong Provincial Department of Industry and Information Technology industry survey).

This means that **for every 6 packaging products produced globally, 1 comes from the Pearl River Delta**. This region, covering only 0.4% of China's land area, hosts over **32,000 packaging and related enterprises** (including printing, materials, and equipment), forming a world-class industrial cluster that spans raw materials, design, manufacturing, and logistics.

So, why do leading global packaging companies — from international giants (like WestRock, DS Smith) to local leaders (such as YUTO Tech, L&P Group) — choose to strategically locate their core production capacity or innovation centers here? Is it a historical accident, or a systemic inevitability? This article will delve into the deep logic behind this phenomenon from six major dimensions: historical policies, industrial chain ecosystem, geographical logistics, talent costs, internationalization level, and future challenges.

II. Historical and Policy Foundations: The "First Testing Ground" of Reform and Opening Up

The rise of the Pearl River Delta began with China's reform and opening-up policy in 1978. As one of the first regions in China to establish Special Economic Zones (Shenzhen, Zhuhai) and open coastal cities, the PRD was at the forefront of undertaking manufacturing transfers from Hong Kong, Taiwan, Japan, Korea, and Europe. Packaging, as the "last link" of manufacturing, naturally followed labor-intensive industries such as electronics, toys, and apparel.

Local governments vigorously supported (supporting industries) through policies such as tax reductions, the establishment of export processing zones, and land preferential policies. For example, in the 1990s, Dongguan proposed the "front shop, back factory" model — Hong Kong took orders, Dongguan produced — giving rise to numerous small and medium-sized packaging factories providing localized services for export goods. This closed loop of "manufacturing — packaging — export" laid the initial advantage of the PRD as a global supply chain hub.

More importantly, policies not only attracted foreign investment but also nurtured local entrepreneurial spirit. Many of today's packaging giants (such as YUTO Tech, L&P Group) started as family workshops and grew into industry leaders under the dual impetus of policy dividends and market demand.

III. Complete Upstream and Downstream Industrial Chain Ecosystem: "Seamless Integration" from Raw Materials to End Customers

1. Highly Synergistic with End-Product Manufacturing

The Pearl River Delta is China's and even the world's most concentrated consumer goods manufacturing base:

Electronics: Huawei, OPPO, vivo, DJI headquarters are all located in Shenzhen.

Home Appliances: Midea (Foshan) and Gree (Zhuhai) account for half of the global air conditioner market.

Fast Fashion: SHEIN's flexible supply chain core is in Panyu and Baiyun.

Toys: Chenghai annually produces over 70% of the world's toys, with its supply chain deeply integrated into the PRD.

These industries demand packaging characterized by **high frequency, small batches, high customization, and rapid iteration**. For example, a new mobile phone launch requires simultaneous development of unboxing experience, anti-counterfeiting structures, and eco-friendly materials. If the packaging factory is thousands of miles away, communication costs and trial-and-error cycles would significantly increase. PRD packaging companies, however, can achieve "customer proposes requirements in the morning, 3D drawings are out in the afternoon, samples are produced the next day," creating strong customer stickiness.

2. Highly Localized Raw Material Supply

Paper Products: Leading enterprises such as Nine Dragons Paper (Dongguan) and Lee & Man Paper (Zhongshan) ensure a stable supply of corrugated paper, white cardstock, and kraft paper.

Plastics: Sinopec Guangzhou Company and Huizhou Daya Bay Petrochemical Zone provide basic particles like PE, PP, and PET; a mature recycled plastic recovery system supports green transformation.

Auxiliary Materials: Inks (e.g., Yip's Chemical), adhesives, and metal accessories (zippers, magnetic clasps) form specialized clusters in Foshan and Zhongshan.

This "half-hour raw material circle" significantly reduces inventory pressure and transportation carbon emissions, enhancing supply chain resilience.

3. Highly Mature Supporting Services System

Mold Development: Dongguan is known as the "World's Mold Capital," with blister molds and injection molds reaching micron-level precision.

Printing and Post-Press: Flexographic, offset, digital printing, hot stamping, UV coating, die-cutting, and other processes are complete, with small and medium-sized enterprises able to outsource as needed.

Design Services: Shenzhen gathers a large number of packaging design companies that understand international brand language, capable of quickly translating marketing concepts into manufacturable solutions.

Logistics and Warehousing: SF Express South China Hub, JD Asia No.1 warehouse, etc., support "same-day delivery" and "next-day delivery."

4. Regional Adaptability for Full-Process Packaging Operations

Packaging, from concept to delivery, involves multiple critical nodes, and the Pearl River Delta possesses unique advantages at each stage:

| Process Stage | PRD Advantage | Example |

|---|---|---|

| Demand Alignment | Concentrated customers, efficient face-to-face communication | YUTO Tech has a customer experience center in Nanshan, Shenzhen, sharing office space with Huawei and DJI |

| Structural Design | Engineers familiar with local equipment and material constraints | Lijia Packaging designers can directly access local paper mill parameter libraries to optimize load-bearing structures |

| Prototyping & Testing | Dense cluster of small CNC, 3D printing, and drop test labs | Dongguan Songshan Lake has over a hundred rapid prototyping service providers, offering 24-hour sampling |

| Mass Production Ramp-up | Equipment clusters + skilled workers, large capacity flexibility | L&P Group's Dongguan factory can scale monthly production from 100,000 to 500,000 units within 7 days |

| Quality Feedback | Engineers can commute to factories the same day, quick issue resolution | An international beauty brand discovered a loose box lid, molds adjusted on-site within 2 hours |

Typical Cases:

YUTO Tech: A global Top 3 consumer electronics packaging supplier, providing AR/VR device packaging for Apple and Meta. Its intelligent factory in Shenzhen integrates AI quality inspection and digital twin systems, leveraging the PRD supply chain to achieve "China design, Vietnam/India replication" for global deployment.

L&P Group: Serves IKEA, Nike, Walmart, emphasizing "green packaging solutions." 90% of its Dongguan base suppliers are within 200 km, resulting in a 35% lower carbon footprint compared to inter-provincial procurement.

Lijia Packaging: Specializes in high-end gift boxes and color boxes, leading in the application of eco-friendly water-based inks and FSC-certified paper, benefiting from local ink and paper supply chains, with delivery times 1-2 days faster than counterparts in the Yangtze River Delta.

LeaflyPackaging: Focuses on medical packaging and cannabis packaging, with proprietary process technology in child-resistant and sealing processes. Benefits from continuous improvement in local manufacturing processes and application of new structural designs, making products popular with customers.

5. Systemic Cost Reduction and Efficiency Improvement from Industrial Clustering: Beyond "Convenience" to a "Revolution in Efficiency"

The packaging industry relies heavily on collaboration, timeliness, and flexible response. The Pearl River Delta, through decades of evolution, has formed a **socialized, networked industrial cluster** that transcends simple geographical aggregation, creating an "industrial operating system." Companies do not need to build entire chains themselves but can efficiently call upon resources within the region through market-based division of labor. This model has led to significant **cost reductions** and **efficiency leaps**.

(1) Theoretical Mechanism: How Do Industrial Clusters Create Value?

According to Michael Porter's theory of industrial clusters, geographical proximity can reduce three types of costs: transaction costs, logistics costs, and information costs. In the PRD packaging industry, the compression of these three costs has translated into quantifiable economic benefits.

(2) Quantifiable Effects: Insights from Industry Surveys and Corporate Practices

| Indicator | PRD Cluster Zone | Non-Cluster Zone (e.g., Central/Western China or Southeast Asia) | Reduction/Advantage |

|---|---|---|---|

| Average Prototyping Cycle | 1–2 days | 5–7 days | Reduced by 60–70% |

| Raw Material Procurement Radius | <50 km | >300 km | Logistics costs reduced by 35–50% |

| Equipment Utilization Rate | 85%+ (shared + outsourced) | 60–70% (self-owned & self-used) | Increased by 20–25 percentage points |

| Order Delivery Cycle (standard color box) | 7–10 days | 15–25 days | Reduced by over 50% |

| Comprehensive Manufacturing Cost (incl. hidden coordination costs) | Baseline 100 | 120–140 | Lower by 20–40% |

Data sources: China Packaging Federation "2023 Packaging Industry Cluster Efficiency White Paper"; L&P Group investor materials (2024); McKinsey "Research on China's Manufacturing Cluster Competitiveness" (2023)

(3) Case Studies: How Cluster Effects Translate into Business Advantages?

YUTO Tech's calculations show that its projects in Shenzhen, due to localized collaboration, have an **NPI (New Product Introduction) cycle 40% faster** than those in its Vietnam factory.

A medium-sized color box factory in Dongguan, by connecting to the local collaboration network, **reduced fixed asset investment by 45%** and increased capacity flexibility by 3 times.

Industry surveys indicate that PRD packaging companies' **average inventory turnover days are 22 days**, compared to the national average of 38 days, freeing up nearly 42% more capital.

(4) Socialized Division of Labor: Small Businesses Can Do "Big Business"

In the PRD, a 10-person design studio can complete the entire process from concept to global shipment by relying on the local supply chain: design → Songshan Lake prototyping → Foshan paper mill supply → Dongguan printing → Guangzhou Port export. This "asset-light, heavy-collaboration" model allows small and medium-sized enterprises to serve top-tier clients like Apple and L'Oréal, **breaking down traditional manufacturing's scale barriers**.

✅ Summary: The value of the Pearl River Delta packaging cluster lies not just in "having everything," but in "extremely fast call times, extremely low costs, and extremely high fault tolerance." This **systemic efficiency**, supported by socialized division of labor and dense networks, is a core competitiveness that cannot be replicated by a single company relocating or building a new industrial park.

IV. Geographical and Logistics Advantages: The "Global Gateway" Connecting Rivers and Seas

The Pearl River Delta boasts one of the world's densest port clusters:

Shenzhen Port (Yantian, Shekou): The world's fourth-largest container port, with dense direct routes to Europe and America.

Guangzhou Port: A hub for domestic and near-sea routes.

Hong Kong Port: Its free port status ensures convenient import of high-end packaging materials.

At the same time, an extensive network of highways (Guangzhou-Shenzhen, Dongguan-Foshan, Nansha Port Expressway), high-speed rail (Guangzhou-Shenzhen-Hong Kong), and airports (Baiyun, Bao'an) forms a multimodal transport system. A finished packaging product can leave a Dongguan factory, reach Shenzhen Port for loading within 2 hours, and arrive in Los Angeles within 48 hours — this "24-hour shipping circle" is a core competitiveness that inland regions cannot replicate.

V. Labor and Technical Talent Reserve: From "Human Sea Tactics" to "Intelligent Manufacturing Upgrade"

In its early stages, the PRD relied on cheap labor, but it has now shifted to a "skills + intelligence" dual-driven model:

Perfected Vocational Education System: Guangdong Light Industry Vocational Technical College, Shenzhen Polytechnic, offer packaging engineering and printing technology majors, supplying thousands of technical talents annually.

High Automation Penetration: High-end printing presses like BOBST and Mark Andy have the highest installed base in the PRD nationwide.

Accelerated Digital Transformation: MES systems, AI vision inspection, and digital proofing platforms are widely used.

This enables PRD packaging companies to handle both high-end orders (such as luxury gift boxes) and efficiently process massive volumes of e-commerce packages, forming a "high-end and mass-market" capability.

VI. Cost and Scale Effects: The "Hidden Dividends" of Agglomeration

Despite rising land and labor costs in recent years, the PRD still maintains a comprehensive cost advantage:

Information Sharing: Frequent industry exhibitions (e.g., China International Packaging Industry Exhibition) and association activities facilitate rapid dissemination of technological trends.

Equipment Sharing: Small and medium-sized factories can rent die-cutting machines and hot stamping machines from larger enterprises, reducing fixed asset investment.

Order Subcontracting: During peak seasons, enterprises can flexibly collaborate, avoiding idle capacity or delays.

More importantly, the "small order, fast response" capability meets the extreme demands of fast fashion brands like Zara and SHEIN for "weekly new arrivals," which is currently difficult for Southeast Asia or India to match.

VII. Internationalization and Market Orientation: Deeply Embedded in the Global Value Chain

PRD packaging companies have been globally oriented since their inception:

Early on, they processed for Hong Kong and Taiwanese funded companies, becoming familiar with international standards (e.g., ISTA transport testing, FSC certification).

Today, they directly serve multinational brands like Apple, IKEA, and L'Oréal, participating in their global packaging strategies.

The explosion of cross-border e-commerce (Temu, SHEIN) has generated massive demand for "lightweight, degradable, branded" express packaging, to which local enterprises quickly respond.

This "export-oriented gene" ensures that the PRD packaging industry always stays at the forefront of global demand.

VIII. Challenges and Future Trends: From "World Workshop" to "Innovation Hub"

Of course, the Pearl River Delta also faces challenges:

Cost Pressure: Some low-end production capacity is shifting to Guangxi, Jiangxi, or even Vietnam.

Stricter Environmental Regulations: Plastic bans and the EU's Carbon Border Adjustment Mechanism (CBAM) are forcing companies to adopt degradable materials and design for reduction.

Technological Upgrades: The need to shift from "manufacturing" to "intelligent manufacturing + services," such as providing full lifecycle packaging management.

But opportunities are equally immense:

Research and development of green packaging (bamboo fiber, bagasse molded pulp) are accelerating.

Digital packaging (AR interaction, NFC anti-counterfeiting) is being piloted in Shenzhen.

The concept of "packaging as marketing" is driving an increase in design value.

In the future, the PRD is expected to upgrade from a "global packaging production base" to a "global packaging innovation and standard output center."

IX. Conclusion

The formation of the Pearl River Delta packaging industrial cluster is by no means accidental. It is the result of the combined action of reform and opening-up policies, geographical location, industrial synergy, market mechanisms, and entrepreneurial spirit. Here, a cardboard from raw material to finished product takes only three days, and a creative idea from sketch to shelf takes only a week — this extreme efficiency is the fundamental reason why global brands choose the PRD.

Looking ahead, only through continuous innovation, green transformation, and digital empowerment can this "packaging hotbed" maintain its irreplaceable position in the global value chain.

Appendix: Summary of Key Data Sources

Global Packaging Market Size: Smithers, The Future of Global Packaging to 2029 (2024)

China and PRD Output Value: China Packaging Federation, Guangdong Provincial Department of Industry and Information Technology (2023–2024)

Enterprise Quantity and Efficiency Data: Qichacha, McKinsey, public company annual reports, industry white papers